MCKESSON (MCK)·Q3 2026 Earnings Summary

McKesson Beats EPS, Raises Guidance as Oncology Surges 57% and AI Investments Pay Off

February 4, 2026 · by Fintool AI Agent

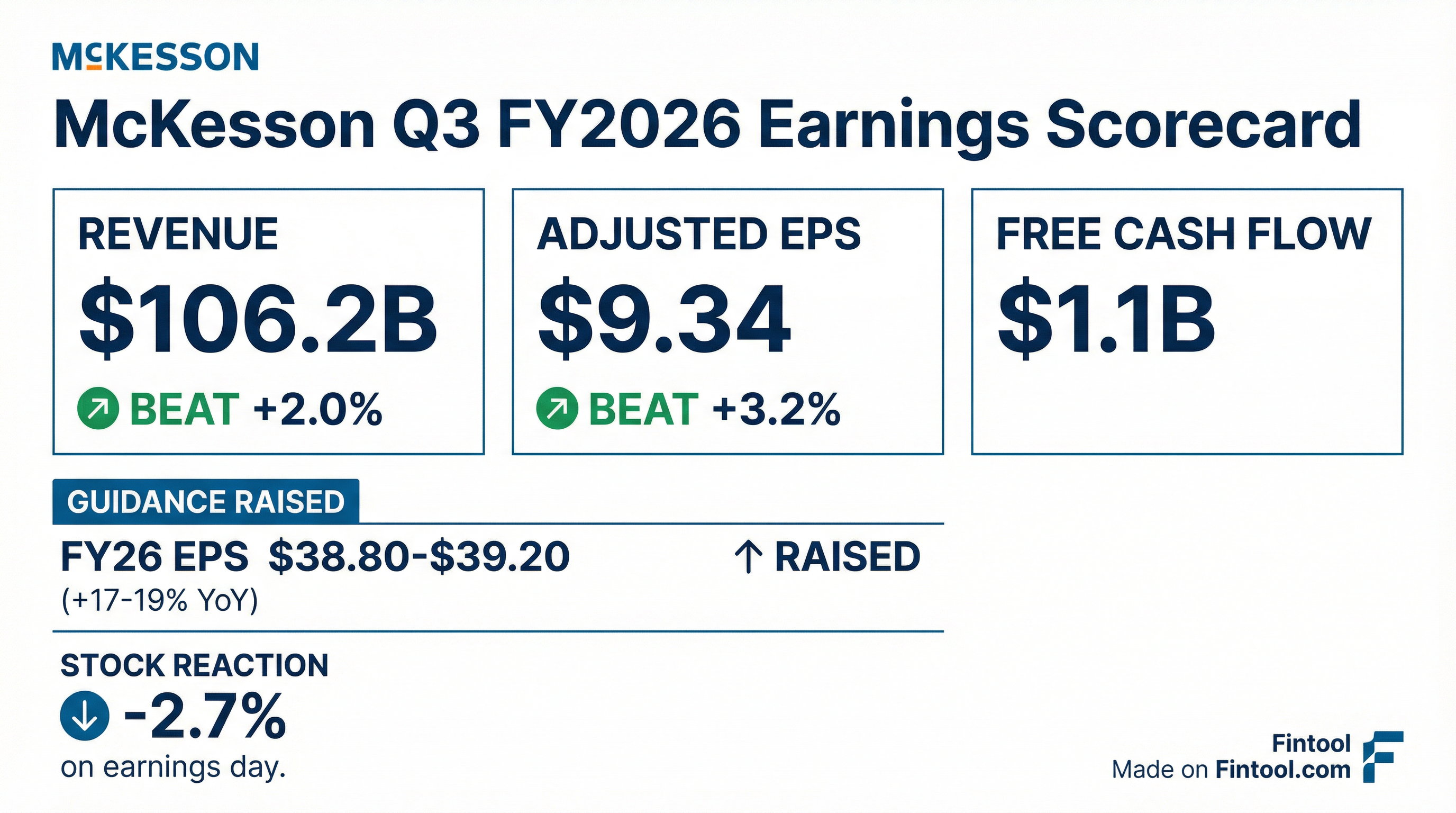

McKesson (NYSE: MCK) delivered a double beat in Q3 FY2026, posting record quarterly revenue of $106.2 billion (+11% YoY) and adjusted EPS of $9.34 (+16% YoY), both exceeding analyst expectations. The healthcare distribution giant raised its full-year guidance, reflecting continued momentum across its core pharmaceutical distribution business and rapidly growing oncology platform. CEO Brian Tyler credited "the strength and durability of our business" and thanked Team McKesson for "unwavering commitment to excellence and innovation."

Did McKesson Beat Earnings?

Yes — both revenue and EPS exceeded consensus estimates.

Values retrieved from S&P Global

Key drivers of the beat included double-digit adjusted operating profit growth in oncology, biopharma services, and North American distribution. The company also delivered a 138 basis point improvement in operating expenses as a percentage of gross profit year-over-year.

What Did Management Guide?

McKesson raised and narrowed its fiscal 2026 adjusted EPS guidance:

CFO Britt Vitalone stated: "We continue to see sustained momentum across our core businesses... The consistency of our strategy, operational execution, and disciplined portfolio management have led to outstanding long-term results."

Segment-Level Guidance for FY26:

What Changed From Last Quarter?

Key developments in Q3 FY2026:

-

European exit complete — McKesson closed the sale of its Norwegian retail and distribution businesses on January 30, 2026, completing its full exit from Europe after a 4-year initiative.

-

Medical-Surgical separation advancing — On January 1, 2026, transition service agreements went into effect. The company continues tracking toward an IPO by H2 calendar 2027, subject to market conditions.

-

AI and automation investments paying off — Each employee is now supporting 120 more patients than last year during the annual verification season, a "meaningful increase in productivity." A new AI chat tool for DSCSA inquiries prevented 75% of inquiries from being escalated.

-

Oncology platform expansion — US Oncology Network now has ~3,400 providers, and PRISM Vision brings together 200+ providers in retina and ophthalmology.

-

GLP-1 momentum continues — GLP-1 distribution revenues hit $14 billion in Q3, up $3 billion or 26% YoY and 7% sequentially.

-

Rite Aid bankruptcy credit — The quarter included a $160M pre-tax credit ($118M after tax) related to the Rite Aid bankruptcy.

How Did the Segments Perform?

*North American Pharma growth impacted by ~3% YoY headwind from prior-year held-for-sale accounting for Rexall/Well.ca divestiture.

Oncology & Multispecialty highlights:

- Organic revenue growth of 24% (excluding acquisitions)

- Organic operating profit growth of 15%

- PRISM Vision and Core Ventures acquisitions contributed ~13% to segment revenue growth

Prescription Technology Solutions highlights:

- Added 50+ new programs across 43 unique brands during the quarter

- Operating margins improved 130+ bps YoY through automation

- Now digitizing enrollment for 1,600+ specialty medications

What Did Management Say About AI?

CEO Brian Tyler emphasized the company's AI and automation investments are driving tangible results:

"Whether we want to call it AI or large language models or generative AI or just other general tech tools, to improve basically the workflows we experience internally... that translated into a big boost in productivity in what, as you all know, is a very person-intensive blizzard season for us."

Key AI initiatives highlighted:

-

Annual verification productivity — Employees supporting 120 more patients per FTE vs. last year

-

DSCSA automation — Built "digitally native from the start" with AI chat resolving 75% of customer inquiries autonomously

-

Canada contact center modernization — Agent assist and enhanced live chat delivering "close to 100% service accuracy and reliability while reducing turnaround time"

-

Patient enrollment digitization — Reducing enrollment time from "days or weeks to sometimes just minutes"

The company is focused on three areas: improving employee experience, enhancing customer/patient experience, and driving efficiency across the enterprise.

Q&A Highlights

On FY27 outlook (Brian Tanquilut, Jefferies): CFO Vitalone pointed to stable utilization trends, strong specialty distribution growth, and 138 bps improvement in operating expenses as percentage of gross profit as "positive building blocks as we move forward into FY 2027."

On oncology segment margins (Lisa Gill, JPMorgan): Vitalone noted that adding Florida Cancer and the PRISM Vision platform are "positive mixed attributes to the segment" and accretive to margins over time. The impact of AI automation "will continue to build over time."

On regulatory environment (Eric Percher, Nephron Research): On IRA Part D, Tyler said McKesson has had "very constructive" conversations with manufacturers about pricing strategies. On MFN: "We think that the way it's rolled out today, it's largely a niche population of cash-paying patients." On Globe (Part B): Tyler noted it exempts existing IRA drugs, applies to only 25% of ZIP codes and 35% of oncology Medicare business — "we don't think it's going to be that material."

On branded drug pricing (George Hill, Deutsche Bank): Vitalone said pricing activity and changes "has been right in line with our expectations... really consistent with what we've seen over the past few years." McKesson has maintained value in manufacturer agreements despite pricing dynamics.

On GLP-1s and prior authorization (Kevin Caliendo, UBS): Tyler acknowledged it's "very early days for the oral GLP-1 launch" but confirmed seeing some prior authorizations come through. The company remains confident the GLP-1 category will continue to grow.

On competitive positioning (Charles Rhyee, TD Cowen): Tyler attributed outperformance to "a clear strategy that's been in place for an extended period of time, a focused management team... some good deployment of capital" with PRISM Vision and Florida Cancer as examples.

How Did the Stock React?

Despite the double beat and guidance raise, McKesson shares closed down 2.7% at $822 on earnings day, though aftermarket trading recovered to $837.50 (+1.9% from close).

Market data as of February 4, 2026

The muted initial reaction may reflect:

- High expectations — Stock near 52-week highs heading into the print

- Medical-Surgical weakness — The -10% profit decline raised questions ahead of planned spin-off

- Soft illness season — Management flagged weak flu season as ongoing headwind

Capital Allocation

McKesson continues aggressive capital return while investing in growth:

CFO Vitalone emphasized: "Our balance sheet is a competitive advantage for us. And it gives us the ability to not only continue to invest back into the business, to acquire assets that are on strategy... but also at the same time to return capital to shareholders."

FY26 guidance includes $2.5B in share repurchases with ~124M weighted average diluted shares.

What to Watch

-

Medical-Surgical spin-off execution — IPO targeted for H2 2027; watch transition service agreement progress

-

Oncology M&A integration — PRISM Vision and Florida Cancer Specialists tracking at or slightly ahead of acquisition case

-

AI/automation leverage — Can productivity gains continue to drive 130+ bps operating expense improvement?

-

GLP-1 trajectory — $14B in Q3 with 7% sequential growth; management expects quarter-to-quarter variability

-

Regulatory environment — IRA Part D, MFN, and Globe policies manageable but require ongoing monitoring

-

Illness season — Soft flu season impacting Medical-Surgical; CDC data showed December severity peak

This analysis was generated by Fintool AI Agent based on McKesson's Q3 FY2026 earnings call transcript dated February 4, 2026. For the full Q3 2026 earnings transcript, visit the document center.